Dubai Real Estate Snapshot – January 2025

Market Overview

Dubai’s real estate market kicked off 2025 strong, with residential values up 1.7% in January and 27% higher year-on-year, albeit with growth slowing in recent months. Villa prices are over 50% above their previous peaks, whereas most apartment values remain about 10% below 2014 highs which illustrates a robust real estate climate inspite of global economic headwinds.

Property Type Breakdown

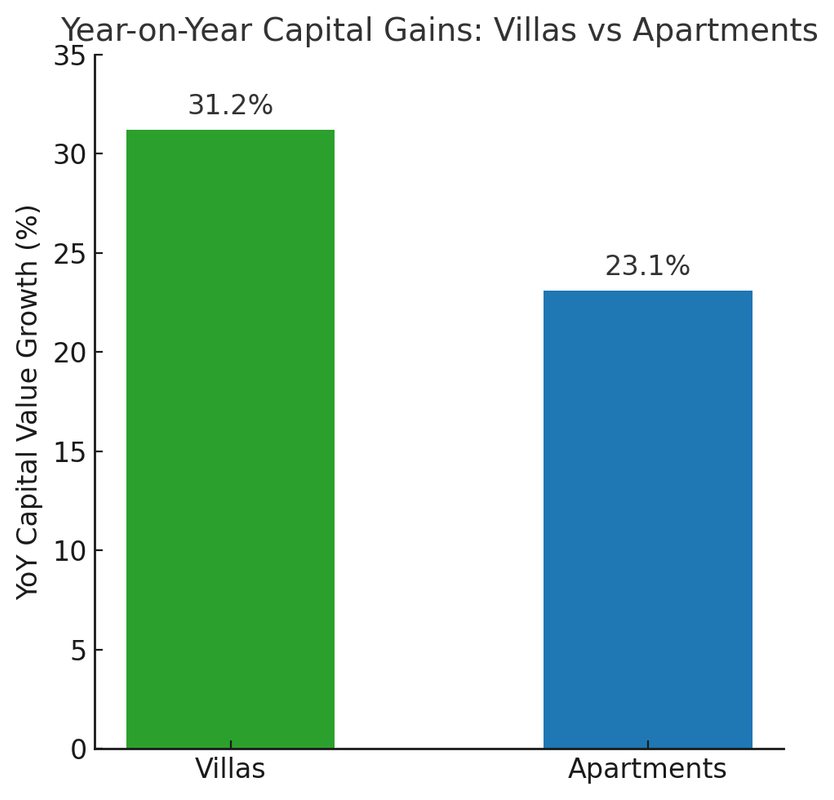

Villas continued to appreciate faster than apartments, roughly 31% vs 23% YoY. In monthly terms, January saw about 2.0% growth for villas and 1.4% for apartments. This signals a gentle cooldown from 2024’s earlier peak pace and a market that is adapting to a more mature growth trajectory.

Villas

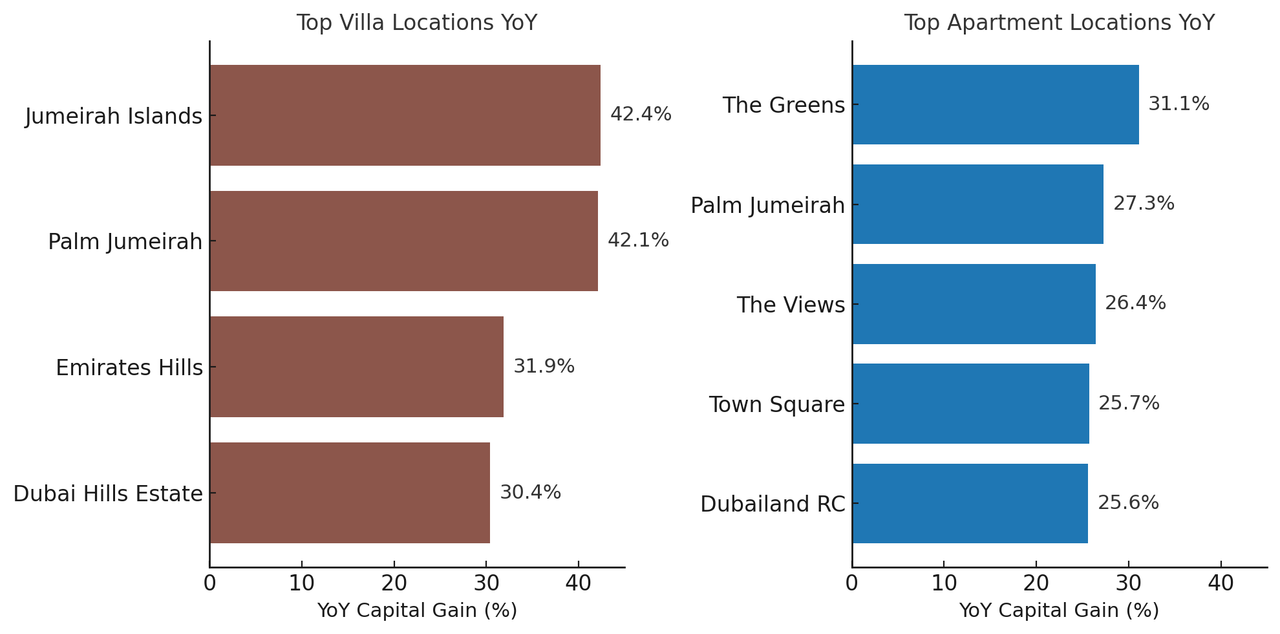

Villas saw the strongest gains, with values up roughly 31% YoY (≈2% MoM). Villa enclaves like Jumeirah Islands jumped almost 42%, whereas growth in some suburban areas was closer to 12%. This reflects a wide range of price growth across villa communities. Jumeirah Islands continues to be a diamond in the rough. Completed almost 20 years ago, the community saw steady growth until a few smart investors saw the implicit value in these villas and started refurbing and selling them for 80-100% more than they bought them for. This kicked off an arms race and other communities such as The Meadows, Springs, Jumeirah Park, Dubai Hills and The Fairways followed suit.

Apartments

Apartments posted about a 23% annual price increase. The top performer as usual was The Greens (+31% YoY), with several popular areas (e.g. Palm Jumeirah) seeing mid-20% gains. Even the slowest apartment segments saw 12-15% growth, and a few prime apartment hubs have now surpassed their 2014 price peaks.

Top locations by annual capital gains. Leading villa districts (Jumeirah Islands, Palm Jumeirah) soared 40%+ YoY, while top apartments (like The Greens) climbed ~30%. Even the fifth-ranked apartment locale saw ~25% annual growth, reflecting broad-based price appreciation.

Sales Transactions

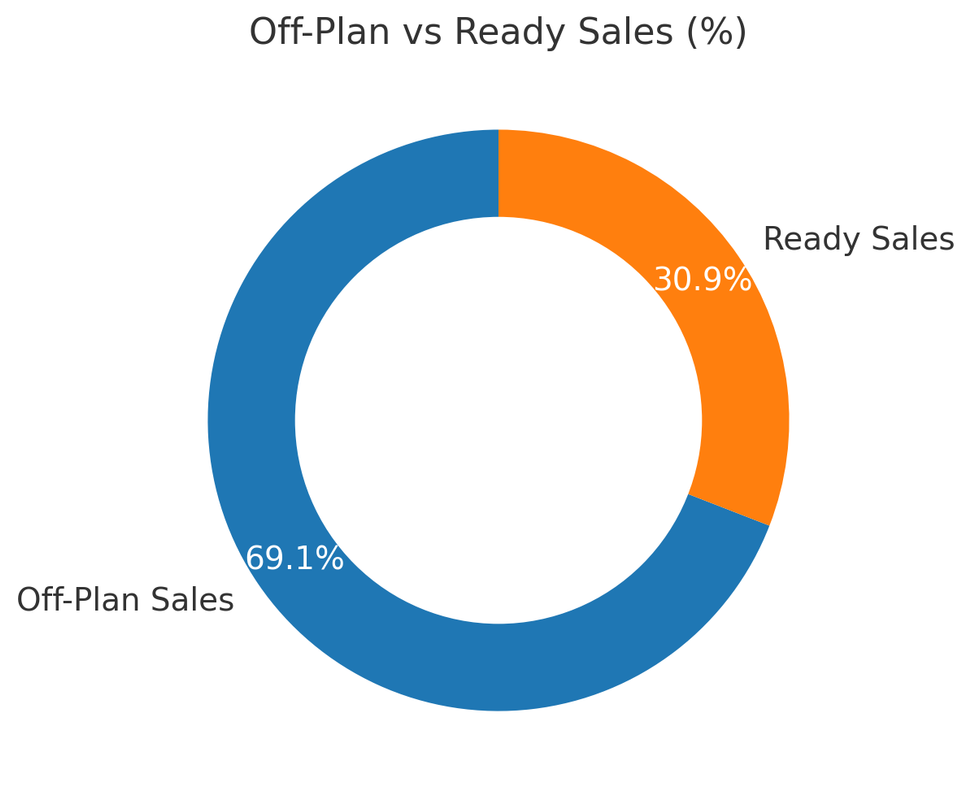

Off-plan sales comprised about 69% of home purchases in January (down from ~71% in December). Off-plan volume fell 13.5% from December but remained 37.9% above last year. Ready home transactions dipped slightly month-on-month as well, but stayed 7% higher year-on-year. January also saw 22 sales over AED 30 million (vs 29 in December), underscoring sustained ultra-luxury demand.

Leading Developers and Locations

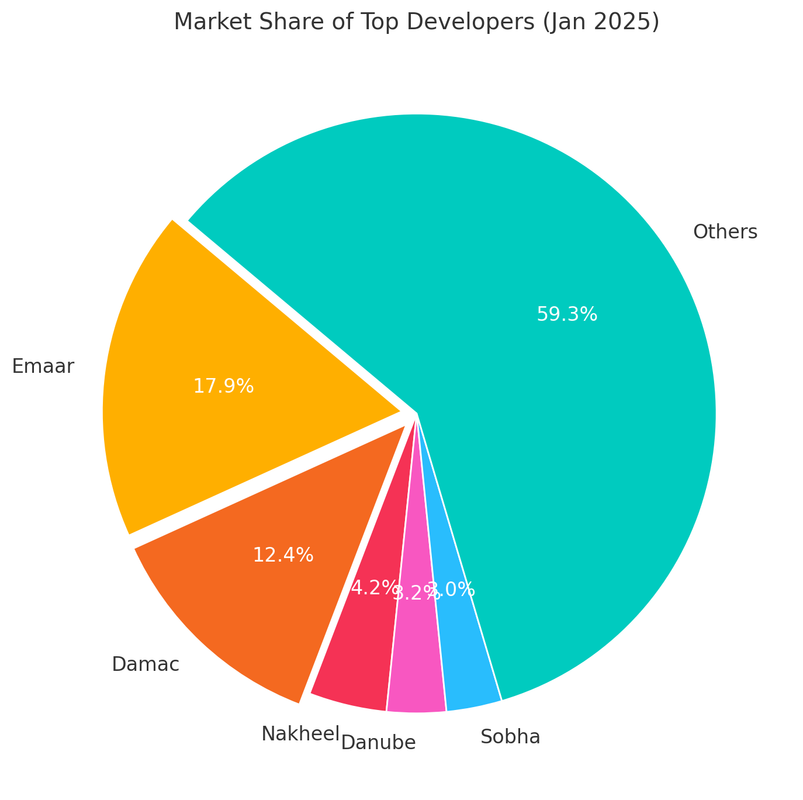

Emaar was the top developer by sales (18% of transactions), followed by Damac (12%). No other developer exceeded 4% of January’s total. Dubai’s busiest areas spanned new and established zones, with Dubailand Residence Complex leading off-plan deals (7.5% of sales) and Jumeirah Village Circle topping ready sales (9.2%). Other active areas included Business Bay and Dubai Marina in the secondary market.

Conclusion and Insights

Dubai’s property market is entering 2025 on a robust yet moderating trajectory. Buyer demand remains strong across off-plan and luxury segments, pointing to continued growth into early 2025 – albeit at a more sustainable pace. This shows that Dubai is adapting to a more sustainable and mature market dynamic and is flexible and adaptable to the current economic climate. As always, keep checking Viewit for the latest news and reviews on Dubai real estate!

Subscribe to our newsletter to stay up to date about the A to Zs of Dubai!